Summary

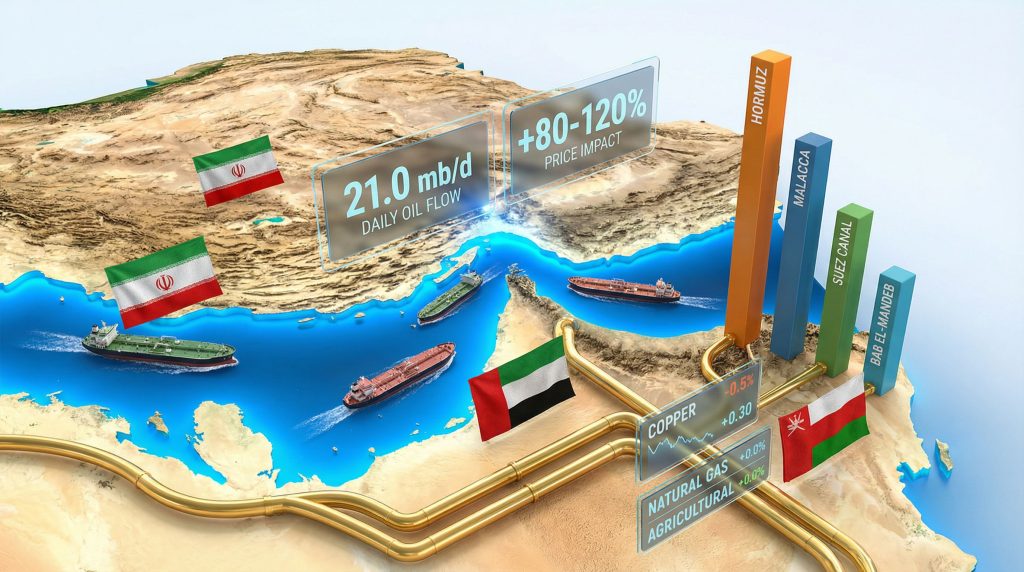

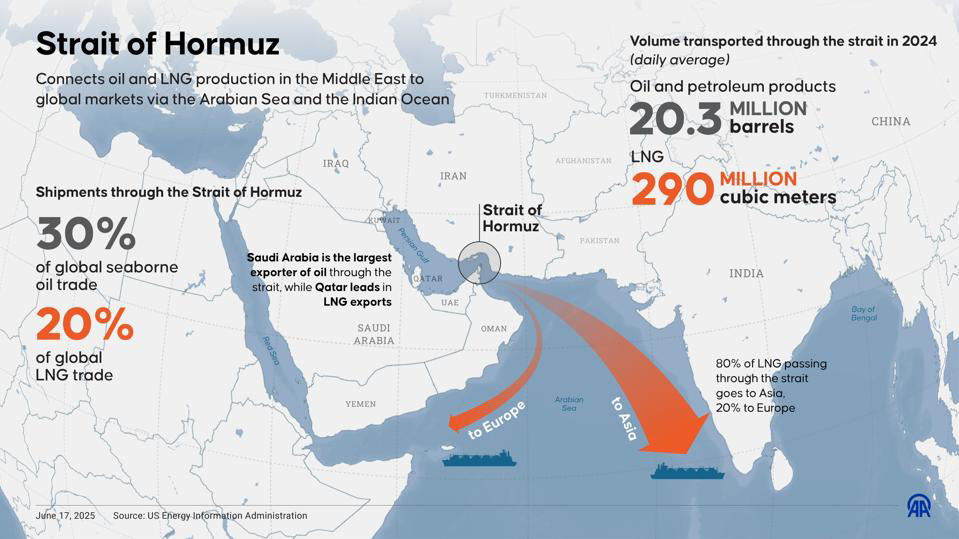

The Strait of Hormuz, a critical global oil chokepoint, carries around 20% of the world’s oil supply. Disruptions in this region ripple far beyond energy markets, significantly impacting rare earth production, logistics, and costs. As China maintains dominance in rare earth processing and global supply chains remain fragile, even minor disruptions can act as a powerful cost multiplier across industries.

Key Takeaways

- The Strait of Hormuz plays a central role in global energy flows and supply chain stability.

- Rare earth production is heavily dependent on energy-intensive processes, making it highly sensitive to oil disruptions.

- China’s integrated dominance in rare earth supply chains gives it strategic leverage.

- Supply shocks can cascade across industries, particularly defense and technology sectors.

- Global diversification efforts are underway but remain years away from maturity.

Disruptions in the Strait of Hormuz significantly impact rare earth supply chains because they increase energy, logistics, and insurance costs, acting as a cost multiplier across the entire production process. Combined with China’s dominance in rare earth processing, these disruptions can trigger immediate price shocks and global supply constraints.

The Invisible Link Between Oil Routes and Rare Earth Supply Chains

Global supply chains are more interconnected than ever before, yet some of the most critical dependencies remain largely invisible to the public eye. One such connection lies between the Strait of Hormuz and the rare earth supply chain—a relationship that underscores how energy flows influence advanced manufacturing and strategic industries.

The Strait of Hormuz, a narrow yet vital maritime passage between the Persian Gulf and the Gulf of Oman, is responsible for transporting nearly one-fifth of the world’s oil supply. This alone makes it one of the most strategically important chokepoints in global trade. However, its significance extends far beyond oil.

Rare earth elements, essential for technologies ranging from electric vehicles and wind turbines to defense systems and semiconductors, rely heavily on energy-intensive extraction and processing. When oil supply is disrupted, the cost of mining, refining, and transporting these materials increases dramatically.

This is why disruptions in the Strait of Hormuz are not just energy shocks—they are systemic cost multipliers that ripple through global supply chains. As geopolitical tensions rise and supply chain resilience becomes a priority, understanding this connection is more important than ever.

Why Does the Strait of Hormuz Matter So Much to Global Trade?

The Strait of Hormuz is often described as the world’s most critical oil transit chokepoint, and for good reason. Approximately 20% of global petroleum liquids pass through this narrow waterway daily, equating to around 20 million barrels per day.

This concentration of energy flow creates a single point of vulnerability. Any disruption—whether due to geopolitical tensions, military conflict, or logistical bottlenecks—can have immediate and far-reaching consequences.

The importance of the strait is amplified by the fact that there are limited alternative routes for transporting oil from major producing regions. This makes the global economy particularly sensitive to instability in this region.

How Do Oil Disruptions Translate Into Rare Earth Supply Chain Costs?

Data-First Section: Energy Dependency in Rare Earth Processing

Rare earth production is not just resource-intensive; it is energy-intensive. Extracting and processing rare earth elements requires significant amounts of fuel and electricity, particularly during separation and refining stages.

Processing costs can account for up to 50% of total rare earth production expenses, with energy being a major contributor. When oil prices rise due to disruptions in key transit routes, these costs increase across every stage of the supply chain.

Transportation costs also surge, as shipping rates and insurance premiums rise in response to geopolitical risks. This creates a cascading effect, where even minor disruptions lead to significant price increases in end products.

Why Are Rare Earths So Critical to Modern Economies?

Rare earth elements are the backbone of modern technology. They are used in high-performance magnets, batteries, and electronic components that power a wide range of industries.

Electric vehicles rely on rare earth magnets for efficient motors. Renewable energy systems, particularly wind turbines, depend on these materials for power generation. Defense systems, including advanced weapons and communication technologies, also require rare earth components.

This widespread dependency means that any disruption in supply has far-reaching implications, affecting not just industrial production but also national security.

How Does China Maintain Dominance in the Rare Earth Supply Chain?

Data-First Section: China’s Market Share

China controls approximately 60–70% of global rare earth mining and nearly 85–90% of processing capacity. This dominance is not limited to extraction but extends across the entire value chain, including separation and magnet production.

China’s advantage lies in its system integration. By controlling multiple stages of the supply chain, it can manage costs, ensure efficiency, and exert influence over global markets.

This integrated approach creates a strategic leverage point. In times of geopolitical tension, export restrictions or policy changes can have immediate global consequences.

What Happens When China Tightens Rare Earth Exports?

When China imposes export restrictions, the effects are felt almost instantly across global markets. Prices can spike sharply as supply tightens, and industries scramble to secure alternative sources.

Defense sectors are often prioritized due to regulatory frameworks such as DFARS, which mandate secure and reliable supply chains for critical materials. This prioritization means that other industries, including consumer electronics and renewable energy, may face shortages or increased costs.

The result is a redistribution of supply that reflects strategic priorities rather than market demand, further amplifying the impact of disruptions.

Why Is This More Than Just a Supply Shock?

Data-First Section: The Cost Multiplier Effect

The concept of a cost multiplier is central to understanding the broader impact of disruptions. Unlike a simple supply shock, which affects availability, a cost multiplier increases expenses across multiple dimensions simultaneously.

Energy costs rise due to higher oil prices. Logistics expenses increase as shipping routes become riskier. Insurance premiums surge in response to geopolitical instability. Each of these factors compounds the others, creating a multiplier effect that significantly raises overall costs.

This dynamic explains why even small disruptions can have outsized impacts on global markets.

When Will Alternative Supply Chains Reduce Dependence?

Efforts to diversify rare earth supply chains are underway, particularly in the United States and allied nations. However, these initiatives face significant challenges.

Data-First Section: Timeline for Capacity Expansion

Domestic rare earth processing capacity in the United States is not expected to reach commercial scale until between 2028 and 2030. This timeline reflects the complexity of building infrastructure, securing permits, and developing technical expertise.

In the meantime, global markets remain heavily dependent on existing supply chains, particularly those dominated by China.

How Are Industries Responding to These Risks?

Industries are adopting a range of strategies to mitigate risks associated with supply chain disruptions. These include diversifying sourcing, investing in recycling technologies, and exploring alternative materials.

However, these efforts require time and capital. In the short term, companies remain vulnerable to external shocks, particularly those linked to geopolitical developments.

Conclusion

The relationship between the Strait of Hormuz and rare earth supply chains highlights a fundamental truth about the modern global economy: everything is connected.

What begins as a disruption in a narrow maritime passage can quickly evolve into a global cost escalation affecting industries, governments, and consumers alike. This interconnectedness underscores the importance of resilience, diversification, and strategic planning.

As the world moves toward cleaner energy and advanced technologies, the demand for rare earth elements will only increase. At the same time, geopolitical risks and supply chain vulnerabilities will continue to shape market dynamics.

Leaders in procurement and supply chain strategy, such as Mattias Knutsson, emphasize the need for forward-looking approaches that prioritize resilience and adaptability. His perspective aligns with a growing recognition that supply chains must evolve to withstand not just disruptions but systemic shifts.

Looking ahead, the challenge is not merely to respond to crises but to anticipate them. In a world defined by complexity and interdependence, the ability to navigate these challenges will determine which economies and industries thrive.

The Strait of Hormuz may be a narrow passage, but its impact is vast—reshaping the economics of critical materials and redefining the future of global supply chains.

FAQs

Why is the Strait of Hormuz important to rare earth supply chains?

Because it affects global oil prices, which directly influence the cost of energy-intensive rare earth production and logistics.

How much oil passes through the Strait of Hormuz?

Approximately 20% of the world’s oil supply flows through this critical chokepoint.

Why does China dominate the rare earth market?

China controls a majority of mining and processing capacity, giving it significant influence over global supply.

What industries are most affected by rare earth disruptions?

Electric vehicles, renewable energy, electronics, and defense industries are highly dependent on rare earth elements.

When will supply chain diversification reduce risks?

Significant diversification is expected closer to 2028–2030 as new capacities come online.