When we look up at the night sky, it’s easy to forget that every star is an ongoing miracle of fusion. Hydrogen atoms collide and fuse, releasing energy that travels across the universe. Without it, we wouldn’t exist. The dream of harnessing that same process on Earth has captivated scientists, engineers, and policymakers for more than half a century. Meet three fusion players reshaping the energy race. From Commonwealth Fusion Systems’ superconducting tokamaks to TAE’s billion-dollar backing and SHINE’s isotope-to-fusion roadmap, discover the promise and challenges of next-gen clean power.

Fusion is more than just another renewable. It is the holy grail: a nearly limitless energy source that produces no greenhouse gases, minimal long-lived waste, and no meltdown risks. If we succeed, it could free us from fossil fuels forever.

But the path is not simple. Fusion requires temperatures hotter than the sun, powerful magnetic fields, and materials strong enough to endure cosmic extremes. For decades, progress has come in careful increments, and skeptics have dismissed fusion as “always 30 years away.”

And yet—something has changed. The last five years have seen fusion leap from scientific curiosity to serious commercial endeavor. Private investment is surging. Governments are issuing roadmaps. Tech giants are signing early power agreements.

At the forefront of this shift are three companies: Commonwealth Fusion Systems (CFS), TAE Technologies, and SHINE Technologies. Each follows a different path. Each faces immense risks. But together, they tell the story of fusion not as a faraway dream, but as a growing industry with timelines measured in years, not lifetimes.

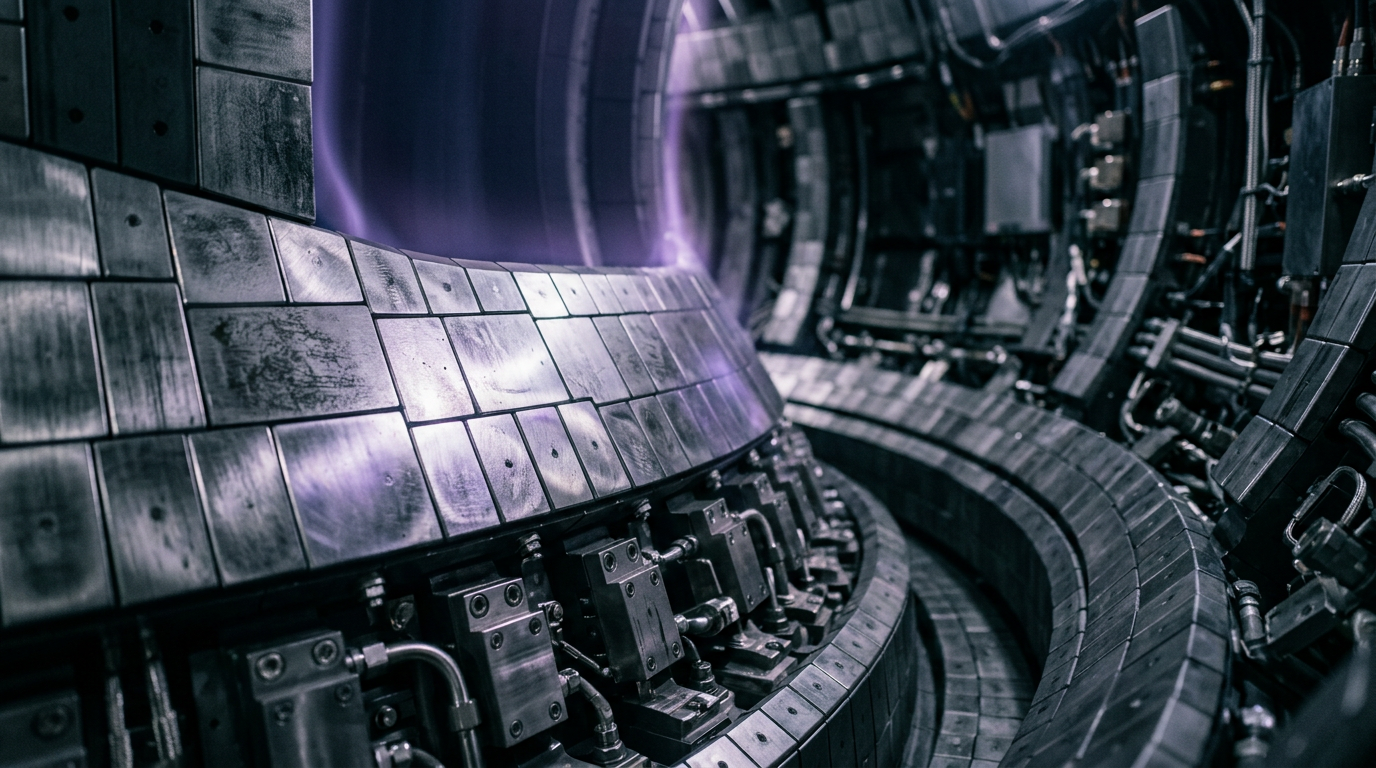

Commonwealth Fusion Players Systems: Scaling Toward the Grid

CFS, a spin-out from MIT, has become a poster child for how fusion can scale with urgency. Their strategy is clear: demonstrate net energy gain with the SPARC tokamak by 2027, then transition to a commercial plant called ARC by the early 2030s.

SPARC is designed to achieve what fusion scientists call Q > 1—producing more energy from fusion than it consumes to maintain the reaction. It’s not just a scientific milestone; it’s the bridge between experiments and power plants.

CFS’s secret weapon is its use of high-temperature superconducting magnets. These allow for stronger, smaller, and cheaper reactors. While older designs like ITER (the massive international project in France) use conventional superconductors and sprawl across entire campuses, CFS’s compact approach promises speed and scalability.

The numbers are bold. CFS envisions ARC delivering around 400 megawatts of clean power, enough for 150,000 homes. They’ve raised more than $2 billion from investors including Breakthrough Energy Ventures, Equinor, and Temasek. In 2023, they completed a 20-tesla magnet test—a world record—that validated their core technology.

And confidence is growing outside the lab. In 2025, Google signed a power purchase agreement for 200 MW of ARC’s projected output, effectively becoming fusion’s first corporate customer. For CFS, this is more than a contract. It’s proof that the private sector is willing to bet on fusion as a real, bankable energy source.

Still, challenges loom. Scaling from SPARC to ARC will test every part of the company’s engineering capacity. Permitting, siting, and supply chains for superconductors must be ironed out. Yet CFS represents fusion’s closest link to the electric grid—a leap from promise to delivery.

TAE Technologies: A Billion-Dollar Bet on Compact Fusion

Where CFS focuses on tokamaks, TAE Technologies has chosen a different path. Founded in 1998 in California, TAE is one of the oldest private fusion ventures. Their goal is audacious: aneutronic fusion using proton-boron fuel instead of the conventional deuterium-tritium mix.

Proton-boron fusion, if achieved, produces virtually no neutrons, meaning far less radiation damage and almost no radioactive waste. But it’s also harder to achieve—it requires plasma temperatures exceeding 1 billion °C.

TAE has moved step by step. Their Norm reactor reached plasma temperatures over 70 million °C—a record for their design—showing steady progress. Their roadmap involves progressively larger machines, with their latest, Copernicus, designed to demonstrate net energy gain within the next decade.

The financial story is equally impressive. By mid-2025, TAE had raised over $1.3 billion, with major rounds led by Google, Chevron, and NEA. In June 2025, they announced another $150 million in funding, signaling continued investor belief even as timelines remain uncertain.

TAE’s strategy goes beyond power. Their spin-off, TAE Life Sciences, applies plasma physics to medical applications, such as targeted cancer therapy. This gives the company near-term revenue streams and builds credibility outside the energy sector.

Skeptics note that TAE has been in the game for decades without yet delivering a demonstration plant. But its persistence, capital base, and scientific vision keep it among the top-tier contenders.

SHINE Technologies: From Medicine to Fusion Power Players

While CFS and TAE aim directly at energy, SHINE Technologies takes a staged approach. Founded in Wisconsin, SHINE first tackled medical isotope production, creating critical materials like molybdenum-99 for imaging and lutetium-177 for cancer therapies.

By mastering isotope production and neutron generation, SHINE is building the industrial and regulatory expertise it will need for fusion. In fact, it already operates one of the world’s largest isotope facilities, supplying hospitals and researchers worldwide.

The plan is stepwise:

- Phase One: Neutron testing for industry and research.

- Phase Two: Medical isotope production—already commercialized and growing.

- Phase Three: Nuclear waste recycling—turning radioactive leftovers into usable resources.

- Phase Four: Commercial fusion power.

This pragmatic roadmap sets SHINE apart. Instead of betting everything on a single breakthrough, they are delivering value today while preparing for tomorrow.

In 2025, SHINE announced expansions in isotope production and new partnerships with defense contractors for neutron applications. Their long-term aim is fusion energy—but unlike some startups, they have revenue and credibility in the here and now.

The Global Landscape: Fusion as a Race

Fusion is not a single-company story. It’s a global race with dozens of players: ITER in France, Helion Energy in the U.S. (which signed a deal with Microsoft), Tokamak Energy in the UK, Proxima Fusion in Germany, and new startups in South Korea, Japan, and Canada.

In 2025 alone, private fusion companies raised nearly $9 billion, according to industry reports. Governments are stepping in too—the U.S. Department of Energy has launched a “Bold Decadal Vision” for fusion, and the UK has invested heavily in its STEP program.

China is also moving aggressively, with its EAST tokamak setting records for sustained plasma, and state-backed firms accelerating fusion materials research.

The landscape is crowded, but that’s a good thing. It reflects diversity of approaches—tokamaks, stellarators, laser-driven inertial fusion, magnetized target fusion—all racing toward the same goal.

Fusion Players Risks and Challenges: The Road Ahead

Despite the excitement, fusion is still risky.

Engineering challenges remain daunting. Building reactors that can handle extreme heat, neutron bombardment, and plasma instabilities is no small feat.

Timelines are ambitious. CFS says early 2030s. TAE aims for late 2030s. Helion claims 2028. History suggests slippage is likely.

Economics are untested. Even if a plant works, will the cost per kilowatt-hour be competitive with solar, wind, or advanced fission?

And public acceptance cannot be taken for granted. Fusion avoids many of fission’s problems, but the word “nuclear” still sparks fear. Regulatory clarity will be essential.

Yet none of these challenges erase the momentum. What has changed in the 2020s is credibility. For the first time, fusion is being backed not just by governments and labs, but by Silicon Valley, Wall Street, and Big Tech. That signals a deeper shift: fusion is now an industry, not a dream.

A Strategic Note from Mattias Knutsson

As Mattias Knutsson, Strategic Leader in Global Procurement and Business Development, puts it:

“Fusion is more than just power. It’s resilience, sovereignty, and vision. Companies like CFS, TAE, and SHINE aren’t just chasing watts. They’re building ecosystems—supply chains, regulatory frameworks, industrial capacity—that will redefine how nations procure and plan for energy. The prize isn’t just kilowatt-hours. It’s independence.”

His perspective reframes fusion. It’s not only about physics, but about strategy—who controls the future of energy, and how they design it into their societies.

Conclusion

Fusion players has been mocked as “forever 30 years away.” But that joke feels increasingly dated. With billions in private investment, corporate power deals, and startups moving from labs to factories, fusion is closer than ever to reality.

CFS shows the grid is within reach. TAE proves persistence and funding can push even the hardest pathways. SHINE demonstrates that incremental progress, grounded in real products, can build a bridge to the stars.

The risks remain huge. But the stakes are larger still. A working fusion industry could deliver clean, endless power to billions, reshape geopolitics, and give humanity a fighting chance against climate change.

And perhaps that’s why the story matters so deeply. Fusion is not just about engineering plasma. It’s about engineering hope. A hope built in labs, funded by bold investors, nurtured by strategy, and sustained by vision.

The dawn of fusion players will not arrive with a bang, but with a hum—the steady sound of reactors turning starfire into electricity, lighting homes, hospitals, and horizons for generations to come.